The weeks, actually months, leading up to November 2024 carried an air of uncertainty for cannabis investors and other interested parties that was evident in the markets. As we drew closer to election day, optimism grew thin, and we could see this in cannabis-related businesses’ (CRB) equity prices (read our October newsletter). And then came Nov. 5, and even worse, Nov. 6. As the results came in, it was as if an anvil were attached to the ankles of every pure play cannabis stock as we watched these companies, once again, get dragged unmercifully to the bottom of the lake.

As we all know by now, the Republicans retained a majority in the House of Representatives while flipping the Senate and the presidency to their side as well. What will follow in terms of cannabis reform is anybody’s guess. However, it was clear that the market didn’t appreciate the election results, not only at the federal level but in the handful of states that had legalization on the ballot (for more on that, see our November Chart of the Month).

Was there any good news on Nov. 5? Sadly, there were no obvious silver linings. With that said, we wouldn’t take rescheduling (or even de-scheduling) off the table just yet. And SAFER Banking has always been more a reflection of Republican ideology than Democratic. But make no mistake about it, any type of cannabis reform is likely to face a steady stream of headwinds as the conservatives are poised to take over in 2025.

Cannabis-linked Equity Performance

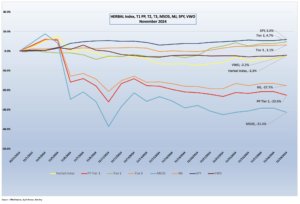

The Nasdaq CRB Monitor Global Cannabis Index (HERBAL), a mix of pure play Tier 1 and Tier 2 CRBs weighted by both investability and strength of theme (SOT), performed well in November relative to its peers (-2.3%), largely due to its security weightings following its semiannual reconstitution in September, specifically its heavier weighting to Tier 2 companies. A full description of HERBAL’s strengths and benefits can be found in Introducing: The Nasdaq CRB Monitor Global Cannabis Index.

The two largest U.S. plant-touching cannabis-themed ETFs, the Amplify Alternative Harvest ETF (NYSE Arca: MJ) (-17.7%) and the actively managed, MSO-heavy Advisorshares Pure US Cannabis ETF (NYSE: MSOS) (-31.4%), were essentially crushed following the November elections. Both of these funds are benchmarked to CRB indexes, and while they use different construction methodologies, their returns will generally be directionally close to each other. Unlike HERBAL, which is an index designed to be Controlled Substances Act (CSA)-friendly, these two funds with U.S. plant-touching MJ exposure tend to be more sensitive than HERBAL to the U.S. regulatory rollercoaster.

MJ’s performance has a high potential to deviate from HERBAL’s (and other cannabis-themed ETPs) due to its current unconventional composition. Since its origin in 2017, MJ has held a significant percentage of non-pure play (and in a few cases, non-CRB) holdings, more specifically tobacco stocks and Tier 3 companies with either very small or no cannabis exposure at all. Additionally in 2022, MJ added and still maintains close to a 50% U.S. plant-touching component via a holding in its sister fund, MJUS. The U.S. plant-touching component also has the potential to impact MJ’s eligibility on investment platforms that restrict U.S. cannabis exposure. It’s also important to note that both MJ and MJUS are now operating under a new issuer, Amplify ETFs.

The performance of the recently expanded CRB Monitor equally-weighted basket of top Pure Play Tier 1 CRBs by market cap was negative in November, returning -4.9%. This basket, which is an equally weighted portfolio of the 21 largest pure play CRBs (including both U.S. plant-touching and non-U.S. plant-touching MJ companies), had a return that was a reflection of the wide range of performance across the entire Tier 1 pure play space. We will take a closer look at some of these below.

The CRB Monitor equally-weighted basket of Tier 2 CRBs significantly outperformed the Tier 1 CRB basket, posting a +4.7% return for November. In February, CRB Monitor published an update to our article on correlations of Pure Play Tier 1 and Tier 2 CRBs (among other tiers and baskets). And what we have observed historically is that these two groups tend to display high correlation (~0.75) in the long term, while their respective performance has a tendency to diverge in the short term. This can be due to (among other factors) the lag from the impact of market forces (like marijuana rescheduling) that affect their sources of revenue that are derived from the Tier 1 group. If this theory holds, investors would be expected to load up on Tier 2 CRBs in the short term, and we would witness this gap narrow over time. We update this data a couple of times per year.

In November, U.S. equities saw a mixed performance, with investors navigating a complex economic landscape that included moderating inflation, resilient corporate earnings, and ongoing concerns about interest rates, as well as the response to the general election. The S&P 500 index remained largely stable throughout the month and closed out November in positive territory. Stocks in the technology sector led the way, buoyed by strong earnings from major players like Apple and Microsoft, as well as optimism surrounding artificial intelligence and cloud computing growth. Meanwhile, cyclical sectors such as consumer staples and utilities faced headwinds, as concerns over higher borrowing costs and potential slowdowns in consumer spending weighed on sentiment. The Federal Reserve’s decision to hold rates steady amid signs of a cooling economy kept markets in a cautious but stable mood. The S&P 500 (represented by the SPDR S&P 500 ETF Trust (NYSE Arca: SPY)) posted a positive 6% return for the month (now +28 % YTD).

Largest Tier 1 Pure Play & Tier 2 CRBs by Mkt Cap – November 2024 Returns

Not surprisingly, an equally weighted basket of the largest Tier 1 pure play cannabis equities got crushed in November. In a continuation of their late October collapse, CRBs plunged in lockstep as the election results became a reality. The silver lining, if there could be one, could be found in the Tier 2 basket (+4.7%), which had a number of winners and appears to be de-coupling from Tier 1 at least in the short term.

CRB Monitor Tier 1

Publicly traded CRB performance was negative (in a few cases, breathtakingly so) in November across the universe of Tier 1 cannabis stocks. The MSO basket generally went into shock, with Tier 1B Cresco Labs Inc. (CSE: CL) (-19.1%), Tier 1B Verano Holdings Corp. (CSE: VRNO) (-56.5% – this is not a typo), Tier 1A MSO Trulieve Cannabis Corp. (CSE: TRUL) (-47.1% also not a typo), Tier 1B TerrAscend Corp. (TSX: TSND) (-22.3%), and Tier 1A Curaleaf Holdings, Inc. (CSE: CURA) (-33.3%) falling back to earth during the month. The largest CRB by market cap, Tier 1B MSO Green Thumb Industries Inc. (CSE: GTII) (-8.8%) did better than its peers in November, but long-term investors in cannabis equities cannot possibly be feeling anything but grief at these returns.

The Canadian CRB basket fared a bit better than the MSOs, likely due to the fact that they operate far away from Florida, from where most of the damage from the election results emanated. As such, returns for Canadian CRBs were mixed in November. As we have stated periodically, historical performance has deviated between the CAD and the MSO baskets over short periods, but the two groups tend to mean revert over time. Canopy Growth Corporation (TSX: WEED) (-14.4%) and Tier 1B Cronos Group Inc. (TSX: CRON) (-1.0%) continued their Q3 slide. Tier 1B craft beverage giant Tilray Brands, Inc. (Nasdaq: TLRY) (-18.3%). We saw positive returns from Tier 1A SNDL, Inc. (Nasdaq: SNDL) (-7.2%) and the big winner Tier 1B High Tide Inc. (TSXV: HITI) (+15.6%) which has been relentless in recent months with its operational expansion across Canada.

CRB Monitor Tier 2

An equally weighted basket of the largest CRB Monitor Tier 2 companies had a positive 4.7% return for November, which outperformed the equally weighted Tier 1 basket by a whopping 27.2%. Typically, these two baskets are highly correlated (please see our February 2024 “Chart of the Month”), and we expect the returns of Tier 1 and Tier 2 CRBs to even out over time. When these two portfolios deviate from one another (as they did in November) a deviation could be a signal for investors to rebalance into (out of) the Tier 1 basket and out of (into) Tier 2’s given their direct revenue relationship, but the precise moment when these two baskets mean revert is not easy to predict. Furthermore, the costs required to systematically rebalance these illiquid baskets could eat up any expected material gains from even the best rebalance strategy. In other words, gaming these two baskets can be a losing strategy, so proceed with caution!

The largest CRB in the Tier 2 basket, popular REIT Innovative Industrial Properties, Inc. (NYSE: IIPR) (CRBM Sector: Real Estate) (-9.9%) recoiled in November but continued its streak of outperformance relative to the Tier 1 CRBs that lease property from them. IIPR’s stock price has consistently outperformed the Tier 1 basket over the last year, having maintained stable earnings throughout a challenging period for the cannabis industry. On Nov. 6, IIPR issued its third quarter 2024 earnings report, which featured the following highlights:

- “Generated total revenues of $76.5 million and net income attributable to common stockholders of $39.7 million, or $1.37 per share (all per share amounts in this press release are reported on a diluted basis unless otherwise noted).

- Recorded adjusted funds from operations (AFFO) and normalized funds from operations (Normalized FFO) of $64.3 million and $57.8 million, respectively.

- Paid a quarterly dividend of $1.90 per common share on November 15, 2024 to stockholders of record as of September 30, 2024 (an AFFO payout ratio of 84%), representing an annualized dividend of $7.60 per common share.

- Sold 402,673 shares of Series A Preferred Stock under IIP’s “at-the-market” equity offering program for $9.6 million in net proceeds.”

Tier 2 REIT Advanced Flower Capital, Inc. (formerly AFC Gamma, Inc.) (Nasdaq: AFCG) (CRBM Sector: Real Estate) (+15.6%) had a strong November, and over recent months it has also outperformed its Tier 1 CRB lending clients. On Nov. 13, AFCG reported its third quarter 2024 earnings of $7.2 million which featured the following statement from CEO Daniel Neville:

“We are pleased with the strong quarter, driven by our continued focus on active portfolio management and origination. One of my top priorities when I joined AFC was to reinvigorate our origination engine, and I am proud to announce that we have surpassed our 2024 target of $100 million in new originations. This achievement highlights our ability to identify and support high-quality operators in key markets, and we look forward to continuing to build on this momentum as we close out the year… On October 15, 2024, the Company paid a regular cash dividend of $0.33 per common share for the third quarter of 2024. AFC distributed an aggregate of $7.2 million in dividends, or $0.33 per common share, compared to Distributable Earnings of $0.35 per basic weighted average common share for such period.”

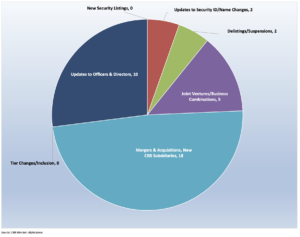

CRB Monitor securities database updates

CRB Monitor’s research team monitors the information cycle daily and maintains securities’ profiles to reflect the current state of the cannabis ecosystem. Here is a summary of the updates for November 2024:

Cannabis business transaction news — November 2024

Election Day clearly grabbed all the attention in November, and as we have written recently, cannabis reform seemed to take a backseat to more pressing issues of the day (inflation, the border, reproductive rights, etc.). Our Chart of the Month digs deeper into the impact from those elections, both state and federal, on the publicly traded cannabis markets. But as they have done over the last decade, these companies continue to provide investors with a news cycle filled with plenty of operational activities to follow.

On that note, here are some of the highlights from November 2024:

Let’s begin in the Great White North, where Canadian Tier 1B High Tide Inc. (TSXV: HITI) announced in a November press release that “its Canna Cabana retail cannabis store located at 1508 Upper James Street, Hamilton, Ontario will begin selling recreational cannabis products and consumption accessories for adult use this week. This opening will mark High Tide’s 187th Canna Cabana branded retail cannabis location in Canada, the 73rd in the province of Ontario and the third in the city of Hamilton. Opening in a former GameStop location, this Canna Cabana store will have excellent visibility within Upper James Square, a major shopping centre in Hamilton. With few competitors in the area, this new store features major Canadian discount retailers and several quick-service restaurants. Situated in a corner unit, this store expands the Canna Cabana footprint in the excellent market of Hamilton and is surrounded by a population density of over 150,000 in a 5-kilometer radius.”

This represents the latest in a months-long operational expansion for High Tide. With this acquisition, High Tide now holds, through its subsidiaries, 198 active cannabis licenses in six Canadian provinces.

Next we head down to New Jersey, where Tier 1B MSO Verano Holdings Corp. (CSE: VRNO) issued a November press release announcing the opening of Zen Leaf Mount Holly, “raising the Company’s retail footprint to four dispensaries in New Jersey and 153 retail locations nationwide… Beginning opening day, Zen Leaf Mount Holly will offer an array of exciting doorbuster deals, including buy one get ones, mix-n-matches, and up to 30% off on select Avexia™, BITS™, Savvy™, Verano™ and (the) Essence™ items.”

Verano, which lost essentially half its value when its stock plummeted following the election, does not appear to be slowing down as it expands its operations in the United States. The press release goes on to say, “Zen Leaf Mount Holly adds another convenient location for South Jersey cannabis consumers, in addition to Zen Leaf Neptune, Zen Leaf Lawrence and Zen Leaf Elizabeth. Verano’s operations in New Jersey include a state-of-the-art 120,000 square foot cultivation and processing facility in Branchburg, where the company produces its signature Verano™ Reserve flower, Swift Lift™ pre-roll joints and vapes; (the) Essence™ and Savvy flower, edibles and vapes; On the Rocks™ Live Rosin vapes and extracts; BITS™ low-dose high-function edibles; and Avexia™ RSO, topicals, tablets and tinctures.”

With this latest expansion, Verano Holdings now holds 75 active licenses through its subsidiary businesses across 14 states.

Now we head west to the two great states of Nevada and Minnesota, where the largest CRB by market cap, Tier 1B MSO Green Thumb Industries Inc. (CSE: GTII), issued a November press release announcing “the opening of its landmark 100th retail location, with RISE Dispensary Carson City on US HWY 50 on November 23. In addition, the Company announced the opening of its 101st retail location with RISE Dispensary Brooklyn Park… The two new locations represent the 11th and 8th dispensaries to open in Nevada and Minnesota, respectively.”

Green Thumb, which has been in expansion mode for the last few years, appeared to escape much of the post-election spiral that hammered its peer group, with a November return of about -9%. With regard to GTII’s charitable efforts, the statement goes on to say, “Profits from the RISE Dispensary Carson City on US HWY 50 grand opening will benefit The Boys & Girls Clubs of Western Nevada, an organization that positively impacts young people by providing a safe, structured, and positive environment where they can build relationships with caring adults, participate in fun and engaging programs, learn important skills, make new friends, and develop their talents. Profits from the RISE Dispensary Brooklyn Park grand opening will benefit Metro Meals on Wheels, a mission-driven nonprofit dedicated to providing fresh, nutritious meals to seniors and individuals with disabilities throughout the Twin Cities metro area.”

With these new additions, Green Thumb now holds 95 active licenses across 15 states.

Next, we head across the Atlantic to Germany, where Canadian Tier 1B CRB Tilray Brands, Inc. (NASDAQ: TLRY) is expanding its product offering. In November 2024, Tilray issued a press release announcing “the launch of its first commercial German grown medical cannabis flowers from its Aphria RX GmbH facility. This launch marks the first medical cannabis products to be grown in Germany by Aphria RX under the newly issued medical cannabis cultivation license under MedCanG. On July 15, 2024, Tilray Medical was the first to receive a new cannabis cultivation license issued under MedCanG. This license allows Aphria RX to cultivate and manufacture a broad range of commercially available medical cannabis in Germany. The strains to be grown at this indoor facility have been carefully selected from top performing varieties popular with patients across Canada.”

Through its subsidiary businesses, Tilray currently holds 350 active licenses across 10 countries.

Finally, on Nov. 4, it was announced in a press release that Canadian Tier 1A CRB SNDL Inc. (NASDAQ: SNDL) “has successfully closed its acquisition of the Indiva Group’s business and assets, pursuant to an approval and reverse vesting order granted by the Ontario Superior Court of Justice. The consideration paid by SNDL as part of the Transaction was comprised of a credit bid of all of the indebtedness of the Indiva Group owing to SNDL, the retention of certain liabilities of the Indiva Group, and cash payments sufficient to repay certain priority indebtedness of the Indiva Group and costs associated with the CCAA Proceedings. The estimated value of the consideration is $22.7 million.”

As a Canadian (non-U.S. plant touching) business, SNDL suffered a much smaller impact on its stock prices from the November elections than its U.S.-licensed peers. The press release goes on to include some details of the transaction:

“The Transaction includes Indiva’s 40,000-square-foot production facility in London, Ontario, and a diverse brand portfolio featuring market leaders like Pearls by Grön, No Future, and Bhang Chocolate. With a portfolio spanning seven brands and fifty-three SKUs, Indiva is a recognized leader in cannabis edibles production and the Transaction is set to reinforce SNDL’s role in meeting evolving consumer demands across Canada.”

SNDL’s footprint now expands to include cannabis operations in nine Canadian provinces and 130 active cannabis licenses.

Select CRB business transaction highlights

Officers/Directors highlights

| Company Name | Ticker Symbol | CRBM Tier | Event |

| Agrify Corporation | NASDAQ: AGFY | Tier 1A | Agrify Secures Financing from Green Thumb Industries and Announces New Leadership |

| Vencanna Ventures Inc. | CSE: VENI | Tier 1B | Vencanna Ventures Announces Strategic Progress, Optimization of Operations, and Management Changes |

| SNDL Inc. | NASDAQ: SNDL | Tier 1A | SNDL Appoints New Chief Information Officer and New President, Liquor Division |

| TerrAscend Corp. | TSX: TSND | Tier 1B | TerrAscend Appoints Lynn Gefen to Expanded Role of Chief People Officer |

Select updates to CRB Monitor

| Name | Ticker Symbol | CRBM Action | CRBM Tier/Sector |

| Arborgen Holdings Ltd | NZE: ARB | Move to Watchlist | Tier 3 – Real Estate |

| SFLMaven Corp. | OTC Pink: SFLM | Moved to Watchlist | Tier 3 – Food, Beverage & Tobacco |

| Lycopodium Limited | ASX: LYL | Moved to Watchlist | Tier 3 – Pharma & Biotech |

| Lontrue Co., Ltd. | SZSE: 300175 | Moved to Watchlist | Tier 3 – Food, Beverage & Tobacco |

| Mobilum Technologies Inc. | CSE: MBLM | Moved to Watchlist | Tier 3 – IT Services & Software |

Cannabis news: Regulatory updates

Now that we have had time to digest the election results, we have put together an analysis of the response by cannabis investors. This can be found in our Chart of the Month. Needless to say, the impact on cannabis-related equities was profound and hit investors hard. With that said, the news cycle from the regulatory space rolls on and we are here for it, as always. Here are some of the November highlights:

Let’s begin with the U.S. Federal Government and Nov. 15 story reported by Marijuana Moment , entitled “USDA Won’t Enforce Rule Requiring Hemp To Be Tested At DEA Labs For Another Year Due To ‘Inadequate’ Access For Growers”. This interesting article begins by stating that “The U.S. Department of Agriculture (USDA) is once again delaying enforcement of a rule requiring hemp growers to test their crops exclusively at labs registered with the Drug Enforcement Administration (DEA), citing “setbacks” at the agency that have led to “inadequate” access to such facilities.”

Why is this consequential for stakeholders? What it sounds like to us is that federal government needs to get its act together on hemp testing (as well as all other regulations and restrictions related to hemp) given the evolution of this controversial type of cannabis.

The article goes on to say, “This is the third year in a row that USDA has delayed enforcement of the lab testing policy for hemp required under the 2018 Farm Bill that federally legalized the crop. Growers will still need to follow other testing rules to ensure product safety compliance, but the DEA registration requirement now won’t be enforced until at least December 31, 2025 under the newly extended timeline… Industry stakeholders have consistently criticized the proposed requirement that hemp could only best tested for THC content at DEA-registered facilities. They’ve argued that the limited capacity has led to bottlenecking and that laboratories can conduct the testing just as effectively even if they aren’t certified by the federal drug agency.”

Next we head out west to Nebraska, where a Nov. 6 article in The Cannabis Business Times reported that while Nebraska voters passed medical cannabis legalization measures on Nov. 5, litigation remains ongoing and is likely to continue for months to come. According to the authors, “Voters in the Cornhusker State supported a pair of complementary statutory initiatives to legalize medical cannabis and provide for a commercial market with 71% and 67% majorities on Nov. 5… With 71% support, Measure 437 intends to protect medical cannabis patients and their caregivers from criminal charges and prosecution by legalizing up to 5 ounces of medical cannabis for those with a written recommendation from a health care practitioner. And with 67% support, Measure 438 aims to adopt state law to establish a framework for licensed businesses to provide tested cannabis products to qualifying patients under the authority of the Nebraska Medical Cannabis Commission. Under the measure, the commission is tasked with adopting cannabis industry regulations by July 1, 2025, and awarding licenses for a commercial marketplace by Oct. 1, 2025.”

While these results were great news for stakeholders and a majority of Nebraskans who supported them, there are now ongoing challenges in the courts that will determine the ultimate fate of legal marijuana in the state. We will be monitoring this battle in the weeks and months to come.

Next, we have a wrap up of the election defeats in Florida and the Dakotas, where our very own CRB Monitor News team reported that “Adult-use cannabis won’t be coming to Florida, North Dakota or South Dakota following the defeat of ballot measures on Nov. 5… Legalization in the Sunshine State was hotly anticipated among investors. The way the proposed amendment was written, existing medical operators would have had the first opportunity to sell in the adult-use market. Any licensing of new adult-use operators would have to be approved by the legislature… Third time was not the charm for adult-use supporters in North Dakota and South Dakota as initiatives in those states also failed. In North Dakota, Measure 5, received only 47% yes votes compared to 53% opposed. Proposed by New Economic Frontier, the measure would have legalized adult-use possession, production and sales, as well as limited home cultivation… South Dakota’s Measure 29 would have only allowed adult-use possession and use, as well cultivation of up to six plants per person or 12 per household. Currently, medical patients can grow only two flowering and two non-flowering plants. The initiative was rejected by 56% of the voters.”

This article goes into detail regarding the impact of these election results on several CRBs, and we take a closer look at this in our Chart of the Month.

Finally, on to Minnesota, where an article published by CRB Monitor News entitled “Minnesota Seizes Illegal Products from Hemp Shops” took a deep dive into an issue that has seized the attention of cannabis stakeholders throughout the U.S. Specifically, Minnesota’s Office of Cannabis Management (OCM) is going after shops that have begun selling THC products ahead of next year’s official start to the legal adult-use market. How can this happen?

According to the report: “Recently, the state filed a civil action against the owner of Zaza, which has two locations that sell hemp products in the Twin Cities area. The lawsuits allege that employees at both Zaza Grand Ave. in Minneapolis and Zaza Lake St. in St. Paul, which are not licensed to sell adult-use cannabis, were selling vapes, pre-rolls and flower that contained more than the state’s limit of 0.3% THC or THCA for hemp products. Further, the suit alleges that employees attempted to hide the illicit products from inspectors using a backpack. The legal action, which seeks a court order allowing the state to destroy seized contraband, comes within weeks of the state conducting a lottery for social equity retail licenses. Winners of those lotteries will get the first crack at Minnesota’s emerging adult-use market, while having to contend with competition from existing hemp shops that are possibly blurring legal lines with hemp-derived intoxicants.”

As with other hemp-related violations, we will (along with our CRB Monitor News team) continue to follow this story as questionable hemp-related activities spread across the U.S.

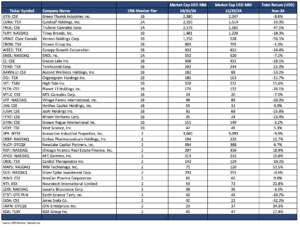

CRBs in the news

The following is a sampling of highlights from the November 2024 cannabis news cycle, as tracked by CRB Monitor. Included are CRB Monitor’s proprietary Risk Tiers.

Wondering what a Tier 1, Tier 2 or Tier 3 CRB is?

See our seminal ACAMS Today white paper Defining “Marijuana-Related Business” and its update, Defining “Cannabis-Related Business.”)