National cannabis reform may be on the horizon, but what would that mean for banks working with an industry that’s already expected to surpass $35 billion in sales in 2025, despite still being federally illegal?

Strict reporting and compliance regulations remain a barrier for many banks interested in entering the space, but as public acceptance of state-legal cannabis continues to grow, so too does the demand for financial services within the industry.

President Donald Trump brought marijuana rescheduling back into the national conversation on Aug. 11 when he said his administration was actively considering a change that would loosen restrictions on cannabis under the Controlled Substances Act (CSA).

“I think that the tea leaves are pretty clear here,” said Saphira Galoob, executive director of the Cannabis Financial Industry Group. “This administration has acknowledged publicly, and we’ve talked with the administration privately: They’re really looking at this issue comprehensively.”

Today, cannabis is classified as a Schedule I drug under the CSA, which is reserved for drugs with no “currently accepted medical use” and a high potential for abuse.

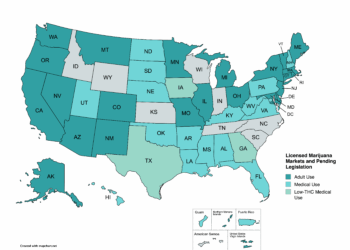

The Department of Justice (DOJ) is currently considering a move to Schedule III, which applies to drugs with low or moderate potential for abuse or dependency. While this would largely leave the recreational or adult-use markets without federal respite, there are still 42 states that allow medical cannabis in some form.

However, the House Appropriations Committee approved a measure covering Commerce, Justice, Science, and Related Agencies on Sept. 10 that would prevent funding to the DOJ for any activities related to rescheduling cannabis. The measure would still need to pass the entire House, but it’s indicative of the ongoing hostility toward legal cannabis among lawmakers.

“Medical is a very big business,” said Erin O’Donnell, founding partner of the Association for Cannabis Banking. “A lot of states are medical only, so I think it would definitely strengthen the lending aspect in banking.”

Compliance requirements may loosen

Rescheduling would not immediately change federal reporting requirements for banks that provide financial services to the weed industry, but it would lead to new regulatory guidance from the Financial Crimes Enforcement Network (FinCEN). This would benefit those already serving the industry and could pave the way for new financial institutions to enter the space.

“There are hundreds of banks currently servicing regulated cannabis companies who are compliant with state laws and they’re doing so despite this current conflict with federal law and they’re doing so because of the Cole Memorandum and FinCEN guidance,” said Galoob.

“I think we will see some smaller regional banks jump in, but I think it depends on how much compliance requirements are involved and what the capital and human expense is going to come from jumping into the segment,” added Paul Evangelista, executive vice president and director of specialized banking at Needham Bank.

After voters in Colorado and Washington legalized cannabis adult-use in 2012, former Deputy Attorney General James Cole issued the so-called Cole Memorandum in August 2013. The memo stated that the DOJ would no longer use any of its resources to enforce federal laws prohibiting the cultivation, sale and possession of cannabis in states where the underlying activity was protected by state law. If the state said you can buy and use weed, the DOJ will look the other way.

Following in the footsteps of the Cole Memo, FinCEN issued guidance in 2014, laying out how banks and credit unions could work with state-legal cannabis businesses without having to worry about a crackdown from the federal government.

Currently, banks are required to file suspicious activity reports (SARs) and follow the Bank Secrecy Act and anti-money laundering guidelines to ensure businesses are not allowing cannabis revenue to go to criminal enterprises and are not covering for criminal activity.

To those ends, banks must perform due diligence and regularly file one of three types of SARs: Marijuana Limited reports for businesses with no red flags, Marijuana Priority when there is evidence of potential wrongdoing, and Marijuana Termination when the financial institution has terminated the account of a cannabis business.

Attempts to legislate a safe harbor for cannabis banking, such as the SAFER Banking Act, have repeatedly failed to pass the U.S. Senate, but rescheduling could make the effort more politically viable, according to Galoob.

“Bankers make their decisions based on risk, safety and soundness,” she said. “So for those that are really, really close, it could get them there for a depository service relationship. For people who are currently servicing cannabis industry stakeholders, could that help expand the financial services or product categories that they’re extending, like more loan products? Probably.”

Those stiff requirements may be enough to dissuade the larger national banks from getting involved, but there are many banks already serving cannabis businesses.

Needham Bank began working with cannabis clients in 2022. Three years later, the Massachusetts-based financial institution serves industry clients across 31 different states.

Prior to its involvement with marijuana, Needham Bank served numerous real estate developers and investors. At some point, one of those real estate companies leased space to a licensed dispensary, meaning the loan payments from the landlord were coming from rent collected from a business that was federally illegal.

“That prompted us to have discussions with our regulators,” said Needham Bank CEO and Board Director Joe Campanelli. “What is the responsibility of our bank? So we did a lot of research around it, talked at the board level and felt that it’s a legal enterprise, and therefore we should be banking it.”

Banking cannabis has been a challenge for at least as long as it could be legally purchased from a storefront instead of the street corner. The lack of options for depositing cash was a major problem in Colorado when the state launched the nation’s first non-medical market in 2014.

“We had seen what had happened in Denver where you have the safe houses, basically single-family and two-family homes that are boarded up from the inside, with cash stacked from floor to ceiling. Our board determined that it was for the safety of the community that we should enter into the space and provide banking services for this industry,” said Evangelista.

Evangelista previously worked for Century Bank and helped launch its cannabis services after Massachusetts legalized medical cannabis in 2012. Eventually Eastern Bank acquired Century, and partitioned off its cannabis business, selling it to Needham Bank.

Financially stronger businesses could attract banks

Evangelista and Campanelli agreed that rescheduling would bring a boost in capital for the industry, along with an even greater need for financial services.

Section 280E of the Internal Revenue Code forbids deductions or credits for business expenses when that business involves illegally trafficking a Schedule I or II drug. The first immediate impact of rescheduling would be that medical cannabis companies could write off business expenses.

“With the removal of the 280E tax issue the operators that the banks and credit unions serve would become stronger. Their balance sheets would become better. They’d have more taxes to write off, so those individual companies would strengthen a little bit,” said O’Donnell. “Having cannabis operators get that rate would probably look very attractive to some bank or credit union lenders.”

In contrast, Evangelista was less certain that the financial benefit of removing 280E would be significantly felt by financial institutions.

“If it happens, it will help the industry because they will be able to deduct general business expenses that today they cannot. Some experts have said balances in accounts could go up as much as 30%,” he said. “I think more importantly they’ll prudently pay down some of the exorbitant debts that they have. So the banks aren’t going to realize as much in balances.”

Even so, any increase in available cash could start offsetting the higher overhead costs from working with the industry. It just remains to be seen which banks might be most interested.

“I think the other notion is that the largest banks in the country are going to jump into the space. I’m not convinced of that because there is still going to be requirements from FinCEN for reporting, tracking and monitoring. Even for a large bank like the Bank of America, if they have to put all the infrastructure in for the reporting, there may not be enough revenue generated to pay for that infrastructure,” said Evangelista. “I think that we will see some smaller regional banks jump in, but it depends on how much compliance requirements are involved, and what the capital and human expense will be from jumping into the segment.”

Either way, there is more work to be done before the majority of banks will be comfortable enough to at least dabble in providing financial services to cannabis operators.

“Bankers need to say, ‘Hey, Congress, we’re either going to bank this industry, or we’re not, but we’re not going to bank this industry with one hand tied behind our back and one leg tied up behind us,’” said Galoob.